We share

Otonomos is all about sharing across our client base and community and learning from best practices we see develop in the emerging crypto hedge fund space.

With this in mind, we have created a feature on our homepage that, after submitting your email, will prepare a unique, editable Google doc version of our BVI fund template, straight to your inbox and ready for you to complete.

In what follows, we walk readers through the main part of this template and highlight some areas that deserve special attention.

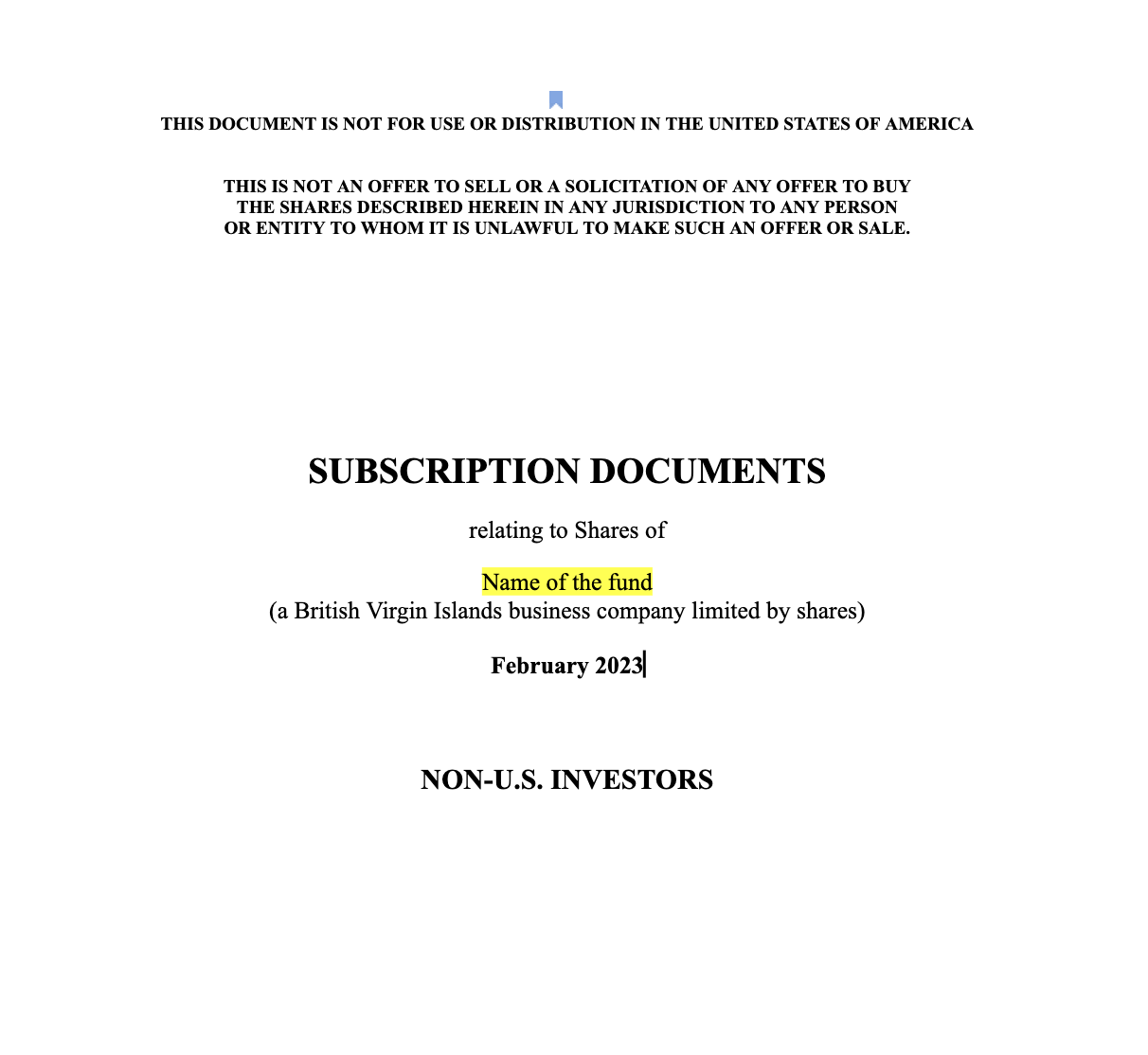

What is commonly referred to as the fund’s term sheet is formally called the Statement of Terms, as can be seen on its cover page.

Our default template caters to non-US investors, as US investors will almost without exception invest via a US feeder (see Part I) in the form of a Delaware LLC which will have its own investor documentation and subscription agreement reflecting substantially the same terms as the non-US term sheet.

The first two page if the template Statement of Terms majorly contain risk disclaimers and regulatory statements.

The Section called “The Fund” is where the Fund’s formal name is specified together with its registered office in the BVI, which Otonomos provides as part of our fund scope of work.

The Section called “Directors” is self-explanatory however as indicated above, it is important that prospective Managers spend some time providing biographic information about themselves.

For the same reasons, the Section called “Investment Objective and Strategy” should have a thorough description of how the Managers plan to go about investing the fund’s assets.

The “Investment Restrictions” of the term sheet are meant to provide an idea - to prospective investor more than anybody else - if the fund will restrict itself from investing in certain assets and/or apply certain strategies.

In this context, it is important to note that an Incubator/Approved fund in the BVI is not restricted from investing in any asset class or from applying any strategies, including leverage. Therefore, this section is more towards prospective investors who may need a degree of comfort about the type of assets the fund can (or won’t) invest in and whether leverage will be applied and if so, how much.

The section called “Minimum Initial Investment” deserves special attention for two reasons:

- In most countries, only so-called “accredited investors” will be able to invest in a fund of this nature, as a result of local offering restrictions on investment products. If the minimum and subsequent investment amounts are set quite high, a non-accredited investor who invests the minimum or more does not become accredited solely on the basis of the size of his/her investment. Reversely, a small minimum investment say US$100 does not cause an accredited investor to lose his/her accreditation, but would still constitute an unregistered offering of securities to non-accredited investors. The minimum amount for a BVI Incubator/Approved fund is US$20,000 and across our clients we see the minimums range from 20k to 100k.

- Secondly, this section makes mention of how this minimum investment can be paid for, an area of particular interest to the crypto community. The types of subscriptions are divided between cash (read: fiat) which should then be paid for by wire transfer, and what is called “non-cash considerations” which, at least in our template, does explicitly include stable coins and other crypto currencies. Stable is perhaps the easiest way to allow for subscriptions, especially if your fund is denominated in US dollars. Any non-dollar linked crypto currency would be more problematic or at least cause more headaches because an exchange rate method would then need to be specified in order to calculate the subscription in dollar terms, if the fund is denominated in dollars. We do not see a lot of funds that are not denominated in dollars, as investors seem to use the US dollar as the reference currency when contemplating a fund’s return, but in principle there is no reason why a fund could not be denominated in e.g. ETH and its returns expressed in ETH.

The “Sponsor Commitment” in the next section touches on what was mentioned earlier regarding Manager “skin in the game” and is more for the comfort of prospective investors who expect Managers to invest a significant amount of proprietary capital in their own fund.

We have a date

The Initial Closing Date is an important concept and is not always well understood.

Essentially, this section asks managers to specify during which period they will raise capital for the fund at a fixed subscription price, before the fund starts making investments. At the Closing Date, the fund will make a tally of how much capital was raised and then decides to (1) either extend the period during which investors can come in at the fixed price, or (2) start making its first investments, as a result of which the NAV will no longer be fixed.

It is important to get this closing date right: you do not want to make the offering period too short so you miss your launch target, but at the same time investors will want to see you deploying the fund’s capital at a foreseeable point in the future because that is what they pay you for. Three months seems to be about the typical period.

The above ties in with the next section called “Additional Closings”:

Additional closings may occur and new Shareholders admitted to the Fund after the Initial Closing Date pursuant to one or more subsequent closings at the discretion of the Board of Directors from time to time, provided that any subsequently admitted Shareholder will subscribe for Shares at the most recently calculated net asset value.

In simple terms, this means that the fund can take on more investors at the NAV per share at the time of their investment.

However, this may need a little bit more explanation. It is not desirable to offer subscriptions and redemptions in the fund on a daily basis or at short frequencies.

This is not so much because it is difficult to calculate the share price of the fund on a day-to-day basis (price feeds are generally available, especially in crypto where every token is basically marked-to-market by the second) but rather because it would make the fund admin rather overwhelming.

A secondary (or perhaps main!) reason is that it is not desirable for Managers to manage “hot money” that could be withdrawn from the fund at very short notice.

Managers rather prefer a stable (read: locked-up) base of capital which they can allocate to conviction trades, however short-term redemptions may force them to sell good positions in order to meet redemption requests.

As a result, we see subscriptions and redemptions frequencies, even for funds that are investing in very liquid tokens, set at quarterly intervals, and only sometimes monthly.

What this means practically can perhaps best be illustrated with an example:

Say a fund puts its subscriptions and redemptions at quarterly intervals. This means that there will be four windows in the year (typically end of March, end of June, end of September and yearend) at which investors can either subscribe for more shares or redeem some or all of their capital by selling shares back to the fund. In this scenario, an investor who would make a subscription say in May would only get to know the price at which (s)he invests at the end of June, and any contributions sent to the fund under a signed subscription agreement would be “parked” until the NAV per share is calculated at the end of June, at which point fresh capital can be deployed. Reversely, any investor who wants to come out of the fund would only be able to do so when a redemption window opens, subject to the withdrawal notices (see section on “Redemptions” below).

The sections called “Share Structure” and “Management of the Fund” have been discussed earlier and the sections on “Management Fees” and “Performance Fees” have been extensively analyzed in our November 2021 Fund Special under its Section E.

The section called “Redemptions” deals with the frequency of redemptions discussed above, and - crucially - specifies how much notice investors need to give when they wish to redeem at the next redemption window.

In the same example above in which the fund has 4 redemption windows at each quarter end of the year, an investor who wishes to redeem say by end of June and is subject to a month’s redemption notice (as specified in the “Redemptions” section) will need to make sure the Manager has been notified latest by end May.

For reason of liquidity management, Managers should aim to get away with the longest possible redemption periods. That way they have ample visibility as to how much money is going to come out of the fund , i.e. how much capital they need to have available at the next redemption window to buy back the shares of the redeeming shareholders.

Because liquidity (mis)management can lead funds to fold, further wording in the “Redemption” section gives Managers the power to “gate” redemptions, with such gates then specified in more detail in the fund’s Memorandum and Articles of Association:

Various other procedural requirements, restrictions and limitations (including the right for the Board of Directors to suspend redemptions in certain circumstances) apply to voluntary redemptions of Shares by Shareholders – please see the Memorandum and Articles of Association for further details.

Finally on redemptions, a manager can impose a redemption fee, specified in the Redemption Fees section of the term sheet, to discourage investors from redeeming frivolously.

Further mechanics

Subsequent sections of the term sheet deal with further mechanics of the fund, the most important ones we highlight below:

The “Term of the Fund” reflects a regulatory requirement to limit the duration of a BVI Incubator/Approved fund to 2 years, extendable to 3 years. Part II of our November 2021 Fund Special has more details on now to then “level up” your fund to a Private or Professional Fund.

The section titled “Custody” leaves it to the Manager to specify how the Fund’s assets will be custodied, and lots of the custody arrangements are typically driven by investors. Under BVI regulations, an Incubator fund and even an Approved fund with assets over US$20MM up to US$100MM does not need to appoint an outside custodian.

The section called “Fund Expenses” simply lists the expenses the Manager is entitled to deduct from the fund’s AUM.

Finally, the Fund may enter into side letters and other agreements and arrangements with certain Shareholders pursuant to which, among other things, a Shareholder may be subject to lower fees or, in respect of employees and persons affiliated to the Fund or its directors, no fees, or pursuant to which a Shareholder may be entitled to receive reports and have access to information regarding the Fund’s investments that might not be generally available to other Shareholders (and the Fund will not be required to provide the same or any similar agreements to any of the other Shareholders)

> Start configuring your term sheet here.